By Andreas Roessler, BackITapp Consulting and Sridhar Rajagopal, Ennoia Technologies

About this article series

This article series explores how O-RAN has evolved in the seven years since the O-RAN Alliance was formed back in 2018, evaluating the differences between its architectural ambitions and what has been achieved so far as the industry moves toward 6G. It reviews significant industry developments through late 2025, including vendor strategies, plugfests and trials, operator rollouts, and emerging initiatives around AI-native RAN architectures that aim to shape the next generation of wireless networks.

Part one provides an introduction and takes the pulse of the industry at the twilight of 2025, heading into 2026. Subsequent parts will examine the state of O-RAN from a technical and commercial perspective, the tension between procurement gravity and innovation, and the growing self-awareness within the O-RAN Alliance as it corrects early architectural gaps, particularly around efficient support for massive MIMO. This leads into a broader discussion of what 6G needs versus what it may get, with a focus on AI-native networks and the role O-RAN plays in enabling or constraining ML-driven performance gains.

Throughout the series, George Axelrod’s 1952 play The Seven Year Itch and Billy Wilder’s 1955 film adaptation serve as a creative lens to examine the persistent tension between aspirational goals and practical outcomes as the wireless industry reshapes its core infrastructure.

Introduction — “The Allure and the Apartment”

Billy Wilder’s 1955 romantic comedy “The Seven Year Itch” portrays a husband, played by Tom Ewell, who, during the heat of summer, envisions an escape from his daily routine through a fantasy confined entirely to his apartment building. Marilyn Monroe’s character embodies this fantasy, which exists as pure possibility—glamorous, unattainable, and most importantly, uncomplicated by the reality of real life.

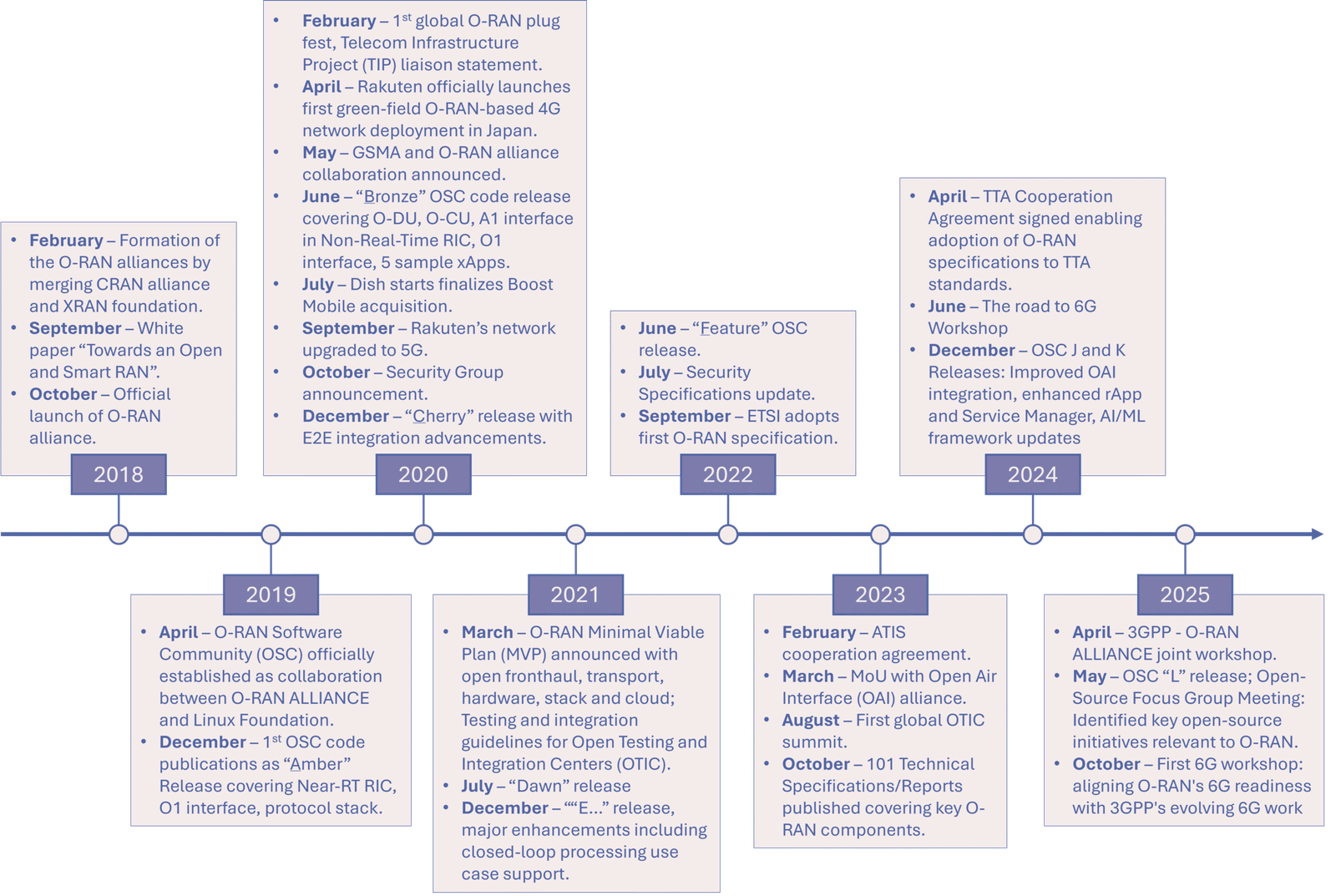

Open Radio Access Network, or O-RAN, was meant to offer a similar escape for the mobile industry. It promised a way out of the suffocating vendor lock-in that had defined radio access networks for decades. Seven years after the O-RAN Alliance was announced in February 2018 and formally established later that year [Figure 1], the vision remains intoxicating: disaggregated RANs, multi-vendor interoperability, innovation at every layer, and costs driven down by competition. The allure is undeniable, almost too perfect to question.

Yet that question now needs to be asked. In early 2026, as the industry publicly celebrates O-RAN’s momentum while quietly watching several of its commercial pioneer’s stumble, it is no longer enough to admire the architecture. Is O-RAN genuinely opening the RAN and fostering a competitive ecosystem, or is it consolidating into another platform-controlled equilibrium as 6G approaches?

The 5G era promised transformation. O-RAN was meant to be one primary mechanism. But somewhere between the lab demonstrations and the profit and loss (P&L) statements, between the interoperability tests at plugfests and live-network demonstrations, a gap has emerged. Not between what O-RAN can technically achieve and what operators hoped for, but between what the architecture enables and what procurement processes and

operational pragmatism ultimately permits. The tension is not about whether openness is possible, but how much openness survives contact with reality.

This examination is not a story of failure. It is a study of how aspiration collides with operational demands, economic constraints, and entrenched industry behavior. Openness, as O-RAN has revealed, is not a property of interfaces alone. It is a sustained commitment expressed through contracts, accountability, data access, and control loops. After seven years of O-RAN development, sufficient evidence has emerged to prompt critical assessment: is this initiative genuinely fostering an open RAN ecosystem, or laying the foundation for a new, more subtle form of centralization that may solidify just as 6G emerges?

That question becomes more consequential as 6G is framed AI-native and cloud-centric, with real-time optimization concepts such as proposed dApps and the E3 message protocol. Control over future RAN platforms will not only shape radio and baseband evolution, but also determine who governs training data, models, and margins over the next decade.

The seventh-year itch is not simply about temptation. It is about whether the industry is prepared to look honestly at what it has built, rather than what it once imagined it was building.

The Pulse of the Industry — “What People Say vs. What They Face”

In Wilder’s film, almost everyone tells themselves a flattering story. The husband insists he is virtuous, the neighbor insists she is innocent, the city insists summer is harmless fun. Reality is more complicated but rarely confronted directly.

Open RAN’s public narrative has followed a similar pattern. In keynotes, surveys, and vendor collateral, it is still framed as a rising tide that will democratize the RAN. In deployment strategy and earnings calls, the tone is more conflicted.

Take Rakuten Mobile – it became the earliest greenfield proof point. In 2020, its executives proudly described their network as the world’s first fully virtualized, cloud-native Open RAN and claimed a cost advantage of roughly forty percent compared to traditional infrastructure [1]. The message was clear: disaggregation, cloud, and automation would overturn legacy economics. Five years later, the picture is more nuanced. By late 2025, the network has served over 9.5 million subscribers with 99.9% population coverage, achieved its first monthly EBITDA profitability in December 2024, and was tracking toward full-year profitability in 2025. The O-RAN path requires extraordinary patience and capital: cumulative operating losses exceeded one trillion yen before the business stabilized. Subscriber growth accelerated throughout 2024-2025, ARPU rose steadily driven by data consumption, and debt was successfully refinanced [2]. Technology worked, but the economics followed only after absorbing losses that few operators could tolerate.

In the United States, Dish Wireless played a similar role. It assembled a multi-vendor network based on O-RAN specifications, with Mavenir, Fujitsu and Samsung as RAN partners and VMware providing the cloud platform [3]. The network hit FCC buildout milestones and even secured a fifty-million-dollar NTIA grant to stand up an Open RAN Integration and Deployment Center (ORCID) that would serve as a living lab for the ecosystem [4]. And yet, by 2025, EchoStar (Dish’s parent) agreed to sell about twenty-three billion dollars’ worth of low- and mid-band spectrum to AT&T and began planning to decommission much of its own access network, pivoting Boost Mobile toward an MVNO-like hybrid model [5]. The network that was meant to validate large-scale multi-vendor O-RAN is now being unwound.

Together, Rakuten and Dish illustrate a consistent lesson. Greenfield deployments can demonstrate technical feasibility, but economic sustainability is neither automatic nor guaranteed. Rakuten showed that O-RAN can scale if losses are tolerated long enough. Dish demonstrated that technical success alone does not protect against market and capital pressures. These conditions are largely unavailable to incumbent operators. A 2025 Fierce Network Research survey found that nearly four out of five industry professionals believe O-RAN is best suited to greenfield deployments, with fewer than twenty-two percent favoring brownfield integration [6]. Established operators must protect existing revenue, maintain service quality, honor long-term contracts, and meet shareholder expectations. They could pursue Rakuten-style transformation only by accepting a level of financial volatility that most governance models simply do not allow. For most incumbents, the cost of leaving familiar ground is higher than the cost of staying put.

AT&T’s trajectory told perhaps the most revealing story. A founding member of the O-RAN Alliance, AT&T spent years advocating for open interfaces and vendor diversification. In December 2023, it announced a five-year, fourteen-billion-dollar agreement with Ericsson for what it described as an “open RAN” deployment [7]. The deal was immediately discussed controversially in the industry. Critics argued it was effectively a single-vendor contract, questioning what was actually “open” about replacing Nokia equipment wholesale with Ericsson equipment. AT&T framed the decision as an operational simplification: one vendor supplying SMO and RAN software, while introducing multiple radio vendors through open fronthaul, including Fujitsu’s 1Finity [8]. If Rakuten demonstrated what multi-vendor Open RAN could be, AT&T demonstrated what it becomes when scale, operational risk, and shareholder discipline are taken into consideration. This was the view from inside the apartment, where responsibility outweighs temptation.

Deutsche Telekom followed a similarly pragmatic path. After extensive O-RAN trials across Europe, the company adjusted its rollout timeline in October 2024, shifting its initial target of 3,000 O-RAN-capable sites in Germany from 2026 to 2027 [9]. This was not a retreat, but a recalibration. By late 2025, those 3,000 sites, using Nokia and 1Finity, were progressing successfully. Yet even here, openness was bounded. Large MIMO deployments remained largely single-vendor (i.e., Nokia) as verification cycles and field validation timelines limited how far multi-vendor integration could realistically extend [10]. Building on these positive outcomes, DT announced plans to issue a request for quotation (RFQ) in January 2026 for about 30,000 sites – set to become the largest O-RAN deployment across Europe [11].

Vodafone’s experience reinforced the pattern. Initially positioned as a European O-RAN leader, Vodafone launched a major RAN tender covering approximately 170,000 sites across Europe and Africa [12]. When results emerged in late 2025, expectations were tempered [13]. Samsung secured the primary O-RAN role in Germany, deploying several thousand virtualized sites, but largely in single-vendor configurations. Ericsson retained dominance across much of Europe and Africa, while Nokia preserved its African footprint. The VodafoneThree UK merger further concentrated investment with Ericsson and Nokia, sidelining earlier Samsung deployments. The original ambition of reaching thirty percent O-RAN penetration by 2030 softened into a more modest, “open-ish” reality. [14].

Mavenir’s journey encapsulated both the promise and peril of the O-RAN ecosystem. Built on a strong mobile core software business that generated roughly ninety percent of its revenue, Mavenir used that financial base to enter the RAN market aggressively in 2020 [15], including the development of massive MIMO radios. Its technical progress was widely acknowledged, with Vodafone’s network leadership praising its energy efficiency advantages over incumbent offerings [16]. Dish’s nationwide deployment over at least 25,000 sites validated true multi-vendor interoperability. Yet market forces proved unforgiving. As RAN spending contracted in 2023 and 2024, operators increasingly segmented networks into single-vendor zones. The capital intensity of radio manufacturing, combined with slow procurement cycles, strained Mavenir’s balance sheet. A June 2025 restructuring eliminated $1.3 billion through a debt-for-equity swap, but also marked Mavenir’s exit from radio hardware, with the dissolution of its radio

engineering team [17]. The retreat was not a technical failure. It was a market verdict on how much innovation the procurement system was willing to absorb.

Governments layered their own narrative onto this landscape. The NTIA’s Wireless Innovation Fund has committed hundreds of millions of dollars to testing facilities, open radio units development, and software innovation, explicitly linking Open RAN to supply chain diversification and national security [18]. These initiatives energized the ecosystem and drew new participants into O-RAN development. Less clear is what happens next. How do these labs sustain themselves once grant funding expires? Who bears long-term integration costs? And do these environments become engines of innovation, or compliance theaters detached from commercial deployment?

What emerges is a tale of two O-RANs. Public messaging still emphasizes transformation and diversification. Field experience tells a more cautious story. Greenfield pioneers proved disaggregation is possible, but not cheap. Brownfield incumbents adopted open interfaces slowly, with extended validation cycles, contingency budgets, and fallback plans that increasingly resembled traditional procurement.

At the same time, O-RAN has found more selective traction in non-public networks, where its architecture aligns with fundamentally different operational requirements than public macro deployments, particularly around scale, mobility, and lifecycle management. Research projects such as Germany’s CampusOS [19] illustrate how O-RAN can reduce 5G operational complexity toward Wi-Fi-like deployment and control models, enabling newcomers and innovators to deliver specialized industrial and mission-critical services. In these environments, O-RAN’s openness also supports interoperability between legacy systems and public 5G for non-critical applications.

The industry’s pulse, beneath the optimism, was elevated. Not panic, but not confidence either. It was the rhythm of an ecosystem that committed to a path and is now discovering, step by step, what that path demands.

Much like the husband in The Seven Year Itch watching Monroe’s character through his window, the industry has spent seven-plus years observing the promise of O-RAN from a safe distance. The question now is not whether the door exists, but who controls what happens after it opens.

In the next part of this series, we move past observation and examine what O-RAN looks like in operational reality, where openness collides with performance, cost, and control.

References

[1] https://www.sdxcentral.com/news/rakuten-mobile-dismisses-open-ran-skeptics (March 3, 2020)

[2] https://global.rakuten.com/corp/news/press/2025/1113_01.html (November 13, 2025)

[3] https://insidetowers.com/samsung-mavenir-accelerate-dish-wireless-buildout/ (February 27, 2023)

[4] https://about.dish.com/2024-01-10-DISH-Wireless-Awarded-50-Million-NTIA-Grant-for-5G-Open-RAN-Integration-and-Deployment-Center (January 10, 2024)

[5] https://ir.echostar.com/news-releases/news-release-details/echostar-announces-spectrum-sale-and-hybrid-mobile-network (August 26, 2025)

[6] https://www.fierce-network.com/premium/research/1409019

[7] https://www.ericsson.com/en/press-releases/2023/12/att-to-accelerate-open-and-interoperable-radio-access-networks-ran-in-the-united-states-through-new-collaboration-with-ericsson (December 4, 2023)

[8] https://www.fierce-network.com/wireless/att-marks-latest-open-ran-achievement-ericsson-1finity (June 20, 2024)

[9] https://www.lightreading.com/open-ran/deutsche-telekom-s-open-ran-plan-slips-after-huawei-reprieve (October 11, 2024)

[10] https://www.lightreading.com/open-ran/deutsche-telekom-plans-30k-site-open-ran-after-nokia-success-vs-huawei (November 5, 2025)

[11] https://www.telecomtv.com/content/the-future-of-ran/deutsche-telekom-preps-rfq-for-30k-ran-sites-54211/ (November 4, 2025)

[12] https://the-mobile-network.com/2023/10/rise-of-the-incumbents-at-fyuz (October 9, 2023) and https://www.techuk.org/resource/fyuz-2023-challenges-and-opportunities-for-open-and-disaggregated-networks.html (October 12, 2023)

[13] https://www.fierce-network.com/wireless/vodafone-finally-names-vendors-its-big-open-ran-deal (October 14, 2025)

[14] https://www.fierce-network.com/wireless/what-does-vodafonethrees-latest-deal-mean-open-ran (September 23, 2025)

[15] https://www.fierce-network.com/tech/mavenir-stokes-open-ran-creates-radio-reference-designs (December 16, 2020)

[16] https://www.lightreading.com/open-ran/mavenir-risks-default-or-restructuring-after-failure-to-crack-5G (November 2024)

[17] https://the-mobile-network.com/2025/06/mavenir-drops-a-billion-in-debt-and-radio-unit-hardware-business/ (June 16, 2025)

[18] https://www.ntia.gov/sites/default/files/2024-05/pwscif-nofo-2-final.pdf (May 2024)

[19] https://campus-os.io/ (January 2026)